Central America Composite Index (CACI) Q2 2026

Introduction

The macroeconomic landscape of Central America in mid-2026 presents a compelling paradox. While the broader emerging market environment continues to navigate tight global credit conditions and shifting international trade routes, the Central American isthmus is demonstrating an unexpected level of internal resilience.

At the Central America Economic Review, we rely on a trusted network of independent academics and institutional data to track these shifts. The latest print of our proprietary benchmark, the Central America Composite Index (CACI), reveals a clear narrative for Q2 2026: domestic resilience, shifting regional leadership, and a structural compression that is narrowing the performance gap between the region’s top-tier economies and its historically trailing nations.

Central America Composite Index (CACI) | Q2 2026 Benchmark

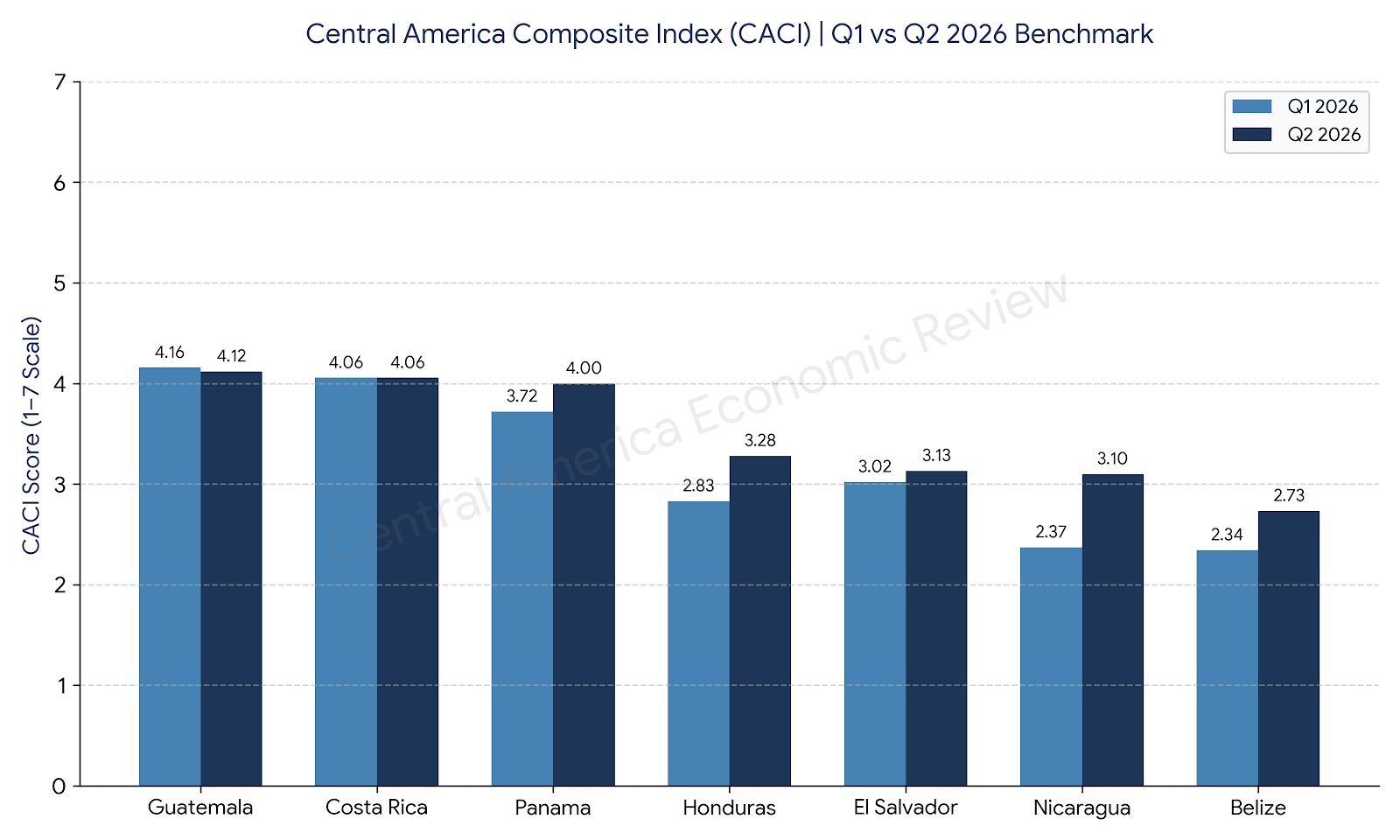

The Q2 2026 Central America Composite Index (CACI) highlights a compelling period of macroeconomic recalibration across the region, characterized by a narrowing gap between historical frontrunners and emerging adapters. While top-tier performers like Guatemala and Costa Rica demonstrated structural stabilization experiencing a negligible pullback and an entirely flat quarter, respectively the true narrative of Q2 lies in the aggressive upward momentum of the lower tiers. Nicaragua led this charge with a sharp +0.73 rebound, followed closely by robust expansionary velocities in Panama (+0.28) and Honduras (+0.45). This collective lifting of the floor reflects notable improvements in localized logistical throughput and risk parity synthesis across the isthmus, signaling a regional transition toward synchronized macro-expansionary velocity heading into the second half of the year.

(Note: The Central America Composite Index (CACI) utilizes a 1–7 scale measuring macroeconomic resilience across Five Foundational Pillars: Structural Integrity, Sovereign Solvency Dynamics, Logistical Throughput, Risk Parity Synthesis, and Macro-Expansionary Velocity.)

The Northern and Southern Anchors: Steady at the Top

Guatemala and Costa Rica continue to anchor the region, maintaining their positions in the Moderate–Strong tier. However, the structural drivers keeping them at the top of the CACI index are fundamentally different.

Guatemala (4.12) experienced a minor 0.04-point correction but retains the highest overall regional score. Guatemala’s placement is a textbook case of "remittance-backed stability." The country’s macroeconomic profile is buoyed by highly conservative banking regulations and robust remittance inflows that support exceptionally strong net foreign asset reserves. This dynamic creates a firm liquidity cushion against sudden capital flight, keeping its Sovereign Solvency Dynamics highly stable despite broader global volatility.

Costa Rica (4.06) remains perfectly flat from Q1, reflecting an economy that is successfully cooling from post-pandemic highs into a more sustainable, long-term phase. Costa Rica benefits from a highly diversified, services-led economy anchored by technology, shared corporate services, and high-value medical device manufacturing. Furthermore, Costa Rica has become a regional leader in sustainable finance, with a growing pipeline of green bonds and sustainability-linked loans.

The primary constraint preventing Costa Rica from breaking past the 5.0 (Strong) threshold remains its Sovereign Solvency Dynamics although theoretically it should move above this level over the next 5 years. Historically elevated public debt levels require ongoing, strict fiscal consolidation. This limits short-term public investment capacity, though structural strengths in education, institutional transparency, and the rule of law continue to heavily outweigh these fiscal rigidities.

Panama’s Transitional Recovery and the Dollarization Advantage

The most significant top-tier movement in Q2 is Panama’s aggressive expansion from 3.72 to 4.00. This marks a vital recapture of investor confidence following the volatility of the past 24 months but was influenced heavily by major macro reporting this quarter as were most of the changes in scores.

Historically the region's gold standard, Panama's risk premium had been pushed into a transition tier following the disruptive closure of the Cobre Panamá mine and the subsequent fiscal slippage that peaked in 2024, which resulted in a sovereign downgrade to speculative grade (BB+) by Fitch. However, the Q2 2026 data indicates that Panama is successfully navigating out of this trough. The government's aggressive fiscal consolidation characterized by narrowing the deficit substantially through 2025 and early 2026 which is stabilizing its macro-expansionary velocity.

Crucially, Panama is benefiting from its unique zero-central-bank dollarized architecture. Because the Superintendencia de Bancos de Panamá (SBP) cannot print U.S. dollars to absorb systemic shocks, Panamanian institutions are forced to maintain structurally higher liquidity buffers than their regional peers. While this binds domestic funding costs tightly to U.S. Federal Reserve yields, it entirely eliminates local currency depreciation and domestic FX volatility. Coupled with a pragmatic energy mix that utilizes thermal generation to backstop its 50% hydroelectric capacity, Panama has engineered a functional resilience that is heavily rewarding its Q2 Logistical Throughput and banking sector scores.

The Lower-Tier Compression: A Narrowing Gap

Perhaps the most compelling structural narrative of mid-year 2026 is the dramatic compression at the bottom of the CACI table. In Q1, the index revealed a deeply bifurcated region. In Q2, the trailing economies surged, significantly narrowing the regional disparity.

Nicaragua (+0.73) posted the largest single gain of the quarter. This sharp rebound is driven heavily by localized improvements in agricultural trade volumes and regional logistics throughput. Despite distinct jurisdictional challenges, Nicaragua’s banking sector has maintained local credit growth, supporting a baseline of domestic commercial activity that lifted its overall Macro-Expansionary Velocity.

Honduras (+0.45) also demonstrated a robust acceleration. A critical driver here is the policy credibility buffer provided by multilateral frameworks. In May 2026, Honduras reached a staff-level agreement with the IMF to complete reviews of its Extended Credit Facility, unlocking approximately $245 million. This agreement reinforces a strict fiscal framework targeting a nonfinancial public sector deficit of just 1.0% of GDP for the year. Backstopped by massive remittance inflows (accounting for over 25% of GDP) Honduras is managing its elevated sensitivity to global tightening cycles better than anticipated, translating directly to its upgraded CACI score.

El Salvador (3.13) and Belize (2.73) also posted gains, though at a more moderate pace. El Salvador remains highly sensitive to U.S. yield increases due to restricted fiscal flexibility, but its retail-driven funding base and push for digital financial inclusion have stabilized domestic deposit metrics.

Rest of 2026 Outlook: Sovereign Spreads and External Pressures

As we look toward the second half of 2026, the Central American isthmus is functioning as a living laboratory for monetary policy. The region hosts starkly contrasting frameworks; from the rigid dollarization of Panama and El Salvador to the crawling pegs and inflation-targeting regimes of Costa Rica and Guatemala. Yet, the Q2 CACI data proves that despite these differences, the baseline of macroeconomic stability is rising across the board. The true test for Q3 and Q4 will be the region's management of sovereign spreads in the face of U.S. Treasury yield volatility and energy shocks. Because global yield spikes translate directly into tighter domestic credit conditions (especially for dollarized or heavily indebted nations). Central America's resilience will depend on maintaining the fiscal discipline demonstrated in early 2026. If governments can balance their sovereign solvency demands with targeted investments in infrastructure and regional integration, the Q2 compression will solidify into a long-term structural upgrade for the entire isthmus.

Author´s Note: The Reality of Regional Macro Reporting

While composite indexes offer a critical framework for cross-border comparison, analyzing Central American macroeconomics requires navigating structurally fluid terrain. Multilateral datasets (including those from primary global institutions) are inherently tethered to self-reported sovereign data, which frequently contends with varying technical capacities and localized reporting lags. Furthermore, regional monetary and fiscal reporting does not exist in a vacuum; data definitions and release schedules can occasionally reflect broader institutional or political crosscurrents.

Recognizing that macroeconomic data globally is built on shifting sand is not a limitation of the CACI framework, but rather its baseline assumption. By synthesizing institutional reporting with localized structural variables, the index aims to cut through the inevitable noise of administrative data adjustments to capture the true underlying velocity of the region's economies.

Subscribe to our Quarterly Economic Brief for country-by-country quarterly breakdowns